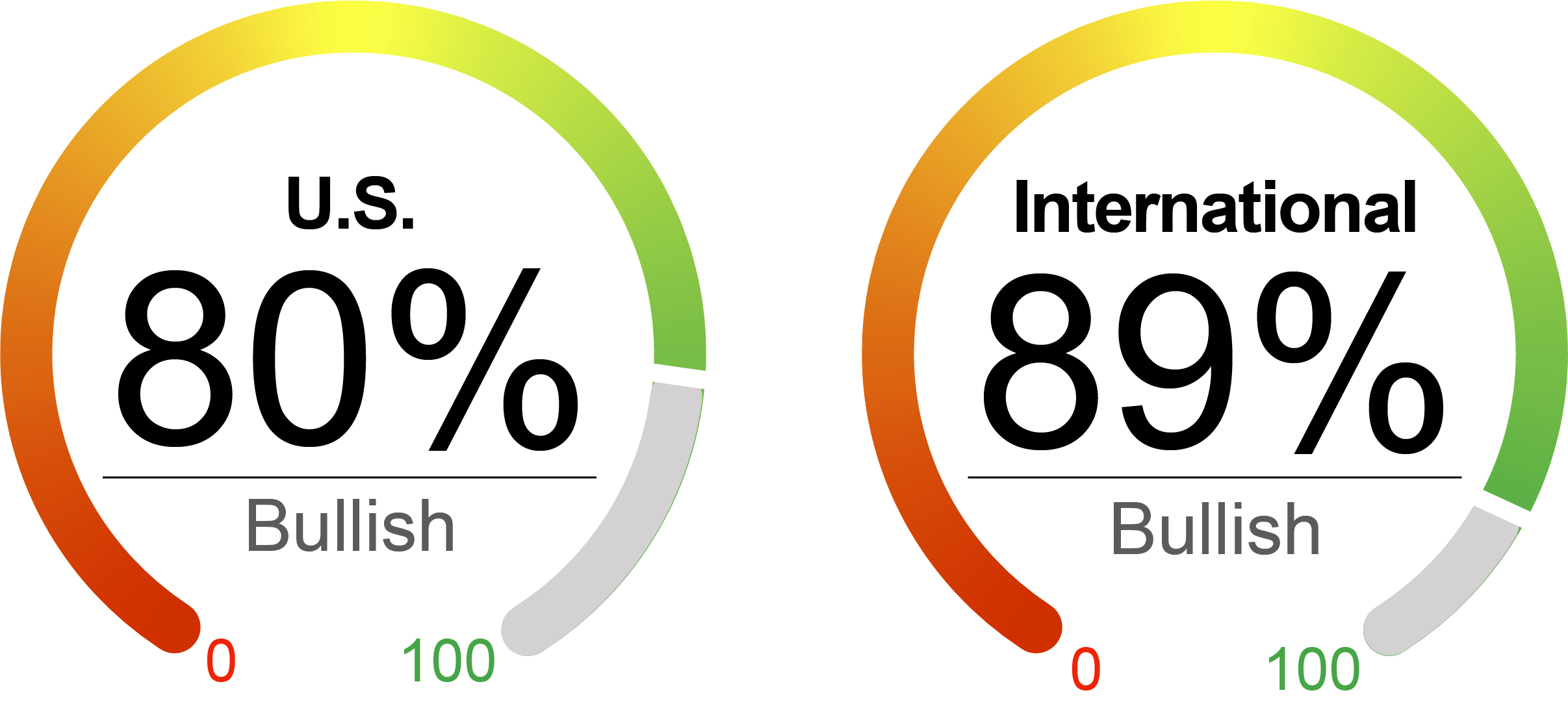

Peaking Momentum, Continuing Solid Growth

The U.S. stock market posted a sixth straight positive month in July with the S&P 500 gaining 2.3%, and the Nasdaq and Dow adding about 1.2% and 1.3% respectively. Utilities, health care, technology and real estate were the top winning sectors in the S&P 500, while energy and financials lost ground. The market was supported by a batch of strong second quarter earnings reports with 88% of S&P 500 companies reporting a positive EPS surprise so far. Notably, the stock market stayed calm after the July Fed meeting, during which the Fed kept its benchmark interest rate near zero. The Fed’s position is that the economy continues to strengthen despite concerns over the pandemic spread.

Over the past few weeks, many investors have been nervously watching the rapid spread of COVID-19 Delta cases in Europe and the western Pacific region as well in several U.S. states. In our view, the economic impact of the virus resurgence would be modest in the U.S. and the Delta variant is not likely to be a serious threat to global growth for at least three reasons. First, widespread vaccination provides protection against severe infections, making another round of lockdown or major policy restrictions less likely in the U.S. Despite the fast rise of new cases recently, hospitalizations and mortality remain relatively low. Second, high frequency data of both mobility and consumer activity have stayed broadly unchanged in the U.S. and only declined modestly in countries such as the UK since the virus resurgence. The global GS Lockdown Index, a combination of official restrictions and actual mobility data, continued to ease over the past month. Other specific metrics such as public transit usage, TSA total traveler, store sales and weekly consumer comfort index have responded little to the new virus cases. Third, even if more aggressive containment measures are introduced, we believe that the economic and corporate profit impact of such measures will be dampened, as economic agents are now more accustomed to restrictions and government supports are expected. Our proprietary COVID model currently indicates a slightly positive score, with decline in the virus-related signals offset by positive high frequency real economy indicators and neutral mobility and financial signals.

The rebound in economic activity remains solid, though, and we see signs emerging that the pace of the U.S. economic growth this cycle may have peaked. While the marginal decline of ISM manufacturing index in June is not concerning, it will likely drop in the coming months, as the index doesn’t normally stay above 60 for too long. The Chicago Fed National Activity Index, a weighted average of 85 indicators of national economic activity, dipped to 0.09 in June. On the positive side, GDP grew at a strong 6.5% annualized rate in the second quarter, boosted by an 11.8% rise in consumer spending as consumers benefited from two rounds of stimulus. Business investment was also robust. Payroll employment gains beat expectations in June. The real estate market has been on a tear, with home sales, homebuilding and homebuilder sentiment surging.

Moving forward, we believe the firm economic backdrop, strong consumer spending outlook and strong corporate earnings should still support the equity market. However, market volatility is expected to rise with the key sources of uncertainty including resurgence of COVID cases, inflation fear, tax policy concerns and the market’s sensitivity to the Fed policy.

|

Negative Indicator |

Neutral Indicator |

Positive Indicator |

Positive Indicator |

|

Valuation With the market hovering around a record high and the S&P 500 index increasing by about 17.7% YTD, valuations for equity are still under pressure. P/E ratios increased to 28.2 at the end of July from 27.7 at the end of June. Forward P/E ratio, on the other hand, fell slightly to 22.3 from 22.7. Inflation adjusted valuation metrics continued to be negative with inflation rising. |

Sentiment Consumer sentiment was mixed with Conference Board Consumer Index flat and University of Michigan Consumer Sentiment Index fell in July. Consumers were encouraged by growing wealth and reductions in restrictions on activity while rising inflation expectation and a high unemployment rate were the major drags. The PMI index dipped but hovered above 60, indicating U.S. manufacturing is holding up well despite bottlenecks in global supply chain and the labor supply issues. |

Technical Technical indicators remained positive but look stretched. At the end of July, the S&P 500 was 12% above its 200-day moving average, 5% above the 100-day average and 3% above the 50-day average. Volatility was on the rise with worries about new virus strains coupled with stretched positioning and light summer trading. VIX index increased to 18.2 compared with 15.8 at the end of last month. |

Macroeconomic Payroll employment rose by 850,000, beating expectations in June. Initial jobless claims were choppy, partially due to seasonal adjustment issues. We expect labor supply constraints to ease with the reopening of schools in the fall and increasing vaccinations, though retiring baby boomers could have a more permanent impact on the labor participation rate. Industrial production rose 0.4%. The real estate market is robust with NAHB homebuilder index remaining at 80 and new private housing climbing to 1.6 million.

|

Important Disclosures